SpaceX didn’t nearly double its revenue in a quarter by launching more rockets. It did it by becoming a compute provider.

Recent IPO disclosures revealed that xAI has agreed to provide Anthropic with large‑scale AI compute services at $1.25 billion per month through 2029. SpaceX generated $18.7 billion in total revenue last year after more than two decades of building rockets—then nearly matched that figure in a single quarter by supplying AI compute.

This isn’t a novelty. It’s a signal.

AI compute has quietly separated from AI model development and emerged as a standalone business category—one large enough to reshape enterprise infrastructure strategy. Analysts now project $7.5 trillion in AI infrastructure spending over the next 4.5 years, roughly 5% of U.S. GDP. That scale of capital deployment hasn’t been seen since the railroad boom of the 1880s.

Enterprise leaders don’t need to become compute providers. But they do need to understand what this shift means for how AI infrastructure is procured, managed, and optimized.

AI Compute Is No Longer Just “Part of the Cloud”

For the last decade, cloud strategy assumed elastic capacity, predictable pricing, and hyperscalers as the default path to scale. AI workloads are breaking those assumptions.

The xAI–Anthropic agreement highlights a bigger change: compute itself is now the product. Capital and innovation are flowing directly into GPUs, high-performance networking, power density, and AI‑optimized storage—not just models and applications.

That shift helps explain what many enterprises are already experiencing:

- GPU availability constraints at major cloud providers

- Rising and increasingly volatile AI workload costs

- Long‑term capacity reservations replacing on‑demand assumptions

The hyperscaler model didn’t fail. It succeeded so well that demand now exceeds what general-purpose cloud infrastructure was designed to support.

The Rise of Neoclouds Signals Structural Change

Markets of this size inevitably drive specialization.

The projected $7.5 trillion AI infrastructure buildout has accelerated the rise of neoclouds and specialized compute providers—companies focused exclusively on delivering AI‑ready infrastructure at scale.

This isn’t fragmentation for its own sake. It’s a response to a simple reality: procurement strategies designed for last-generation cloud economics are misaligned with the economics of AI compute.

Enterprises treating AI workloads as just another line item in existing cloud contracts are discovering that cost, performance, and access no longer behave the way they expect. Infrastructure decisions that once felt operational are becoming strategic.

What This Means for Enterprise Infrastructure Strategy

For enterprise IT and business leaders, the question is no longer whether AI infrastructure matters; it is whether it matters. It’s about engaging with it without locking into outdated assumptions.

Three implications are becoming clear.

First, vendor concentration risk is increasing. Relying on a single provider for AI compute introduces pricing and capacity risk at exactly the wrong time.

Second, AI workloads demand integrated infrastructure thinking. Compute, storage, networking, security, and automation can’t be modernized independently. Bottlenecks surface immediately when one layer lags.

Third, operational management is emerging as a cost differentiator. Two organizations running similar hardware can experience dramatically different economics depending on how they manage their AI infrastructure.

Infrastructure vendors are responding accordingly.

Infrastructure Is Being Rebuilt for the AI Era

Recent platform announcements, including next-generation server and storage releases, reflect a broader shift. Infrastructure is no longer sold as discrete components—it’s delivered as AI‑ready stacks that combine compute, storage, cyber resilience, and automation by design.

The era of piecemeal upgrades is ending. AI workloads expose every weak link, and selective modernization often just moves the constraint elsewhere.

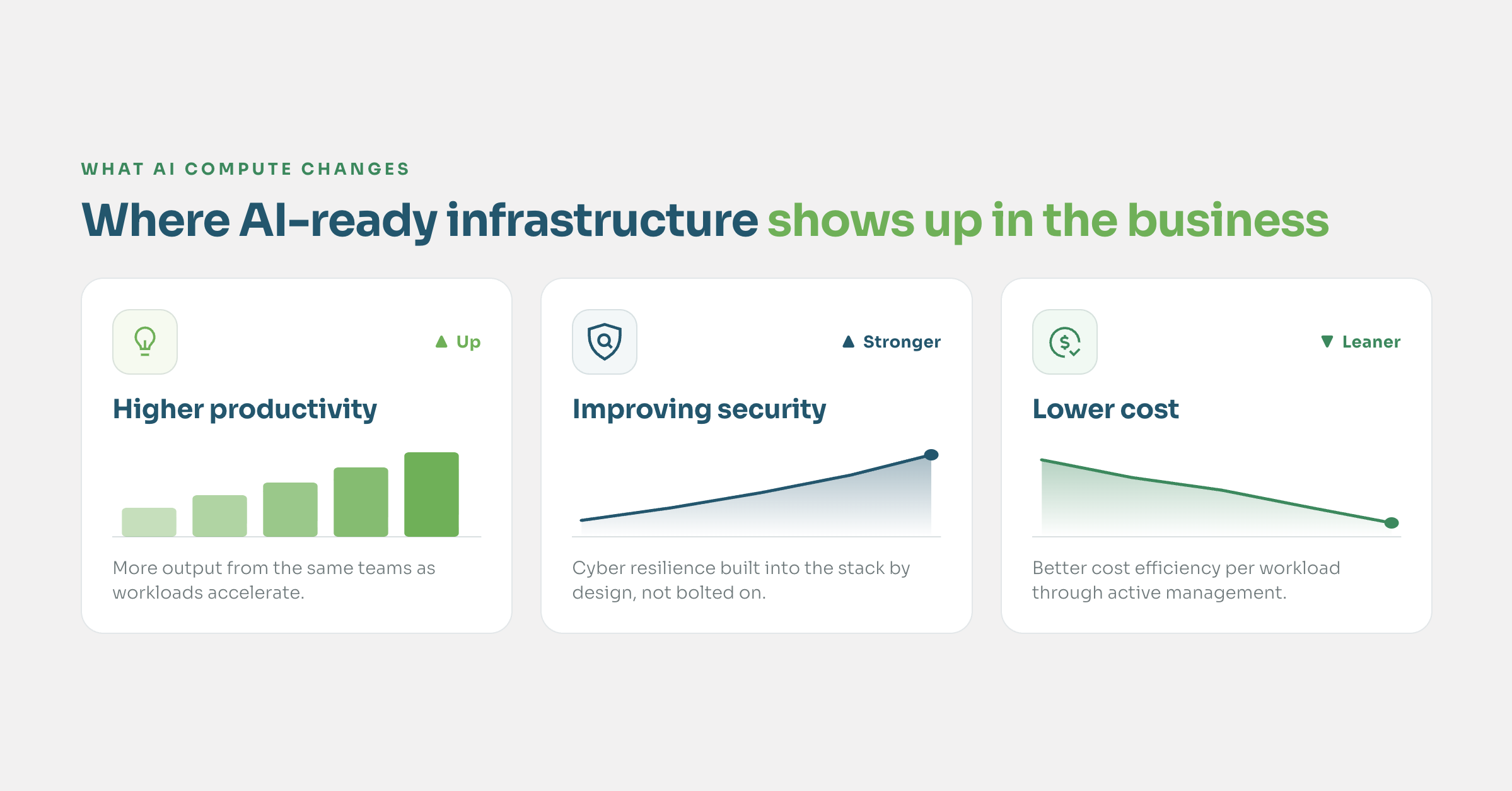

Why Management Will Separate Winners from Laggards

As AI infrastructure economics evolve, management—not hardware alone—will determine who gains a structural advantage.

Organizations that optimize AI infrastructure management over the next 12 to 18 months will operate at lower cost, with greater flexibility, and with less exposure to supply shocks. They’ll be able to balance providers, shift workloads, and adapt as pricing and availability continue to change.

Those who wait will find themselves paying more for less control.

The lesson from SpaceX isn’t that every company should sell compute. It’s that AI infrastructure has entered a new economic phase—one where scale, specialization, and management matter more than legacy assumptions.

Enterprise leaders who recognize this early will be better positioned to compete in an AI‑driven economy.

A Practical Next Step for Enterprise Leaders

As AI infrastructure economics continue to shift, enterprise leaders should take a hard look at how their current AI workloads are sourced, managed, and governed. The organizations gaining an advantage aren’t just acquiring more compute—they’re actively aligning infrastructure decisions to workload economics, risk tolerance, and long-term flexibility.

A useful starting point is a candid review of where AI infrastructure costs, capacity constraints, or vendor dependencies are already limiting momentum. In a market changing this quickly, understanding those gaps early can make the difference between scaling efficiently and paying a premium to catch up later.